Are you shifting your focus towards Inflation and The National Debt? The rally since last March has been driven by progress on COVID, massive amounts of monetary and fiscal stimulus, and optimism on vaccines and the reopening of the economy. The S&P 500 increased by 6.2% in the first quarter of 2021. The main pillars of the rally are still in place as the vaccine rollout and fiscal stimulus could lead to strong economic and corporate earnings growth while the Fed is still committed to maintaining accommodative monetary policy.

Following a year of economic instability, it appears that many of us are turning our attention to the following two topics, which have recently piqued national interest:

Inflation and The National Debt.

Let us discuss these topics in order.

INFLATION:

A recent study found that people are Googling the word “inflation” at a rapid rate, with a peak not seen since 2008.

- The technical definition of inflation is a sustained rise in overall price levels.

- Sam Ewing defined inflation in more practical terms as, “Inflation is when you pay fifteen dollars for the ten-dollar haircut you used to get for five dollars when you had hair.”

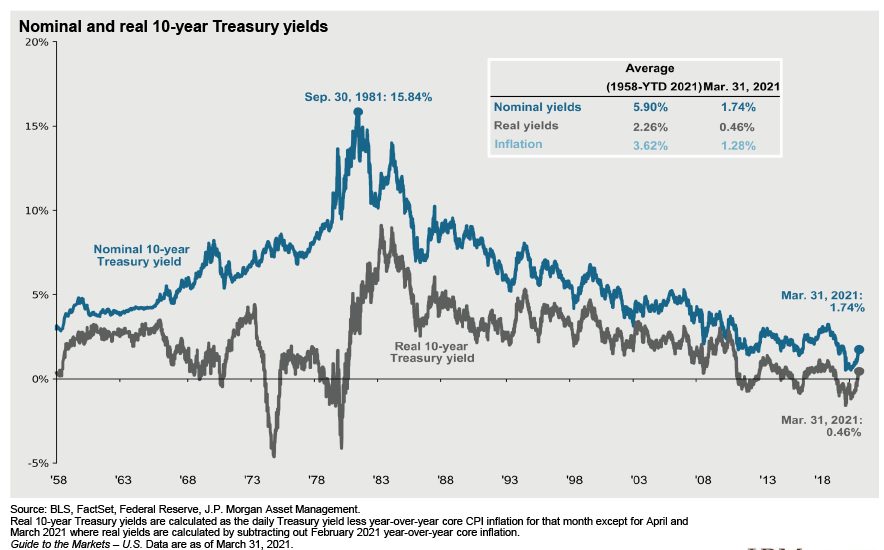

Interest rates and inflation are highly correlated, so a dramatic or sudden increase in interest rates can lead to inflation.

Think of it this way. People consult the level of rates when deciding to buy a new home or refinancing an existing one. Businesses refer to the current level of interest rates for debt and equity financing decisions. When rates rise, we generally pay more for things.

Longer dated bonds have seen quite a move up in their yields (another word for rates). The rate on the 10 Year U.S. Treasury Note has increased from 50 basis points (.5%) in August to over 160 basis points (1.65%) currently. It is important to note that home mortgage rates are often set off the 10 Year note.

- Naturally, this increase in rates has led to nervousness about inflation.

THE NATIONAL DEBT:

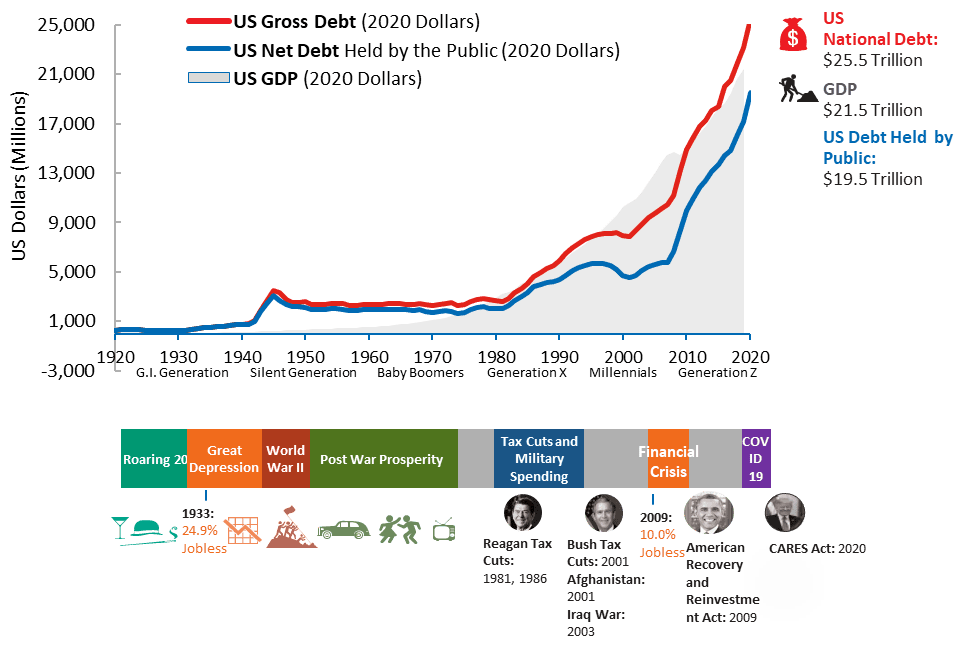

Since the start of the COVID pandemic, six major stimulus bills totaling around $5.3 trillion have passed. With these efforts to alleviate pandemic-fueled financial strife, is the U.S. National Debt Level spiraling out of control?

It is interesting to know that the U.S. debt has steadily risen since the country was founded. Some may see this as a negative sign, but one of the founding fathers and first treasury secretary of the United States, Alexander Hamilton, designed it this way!

WHAT THIS MEANS FOR YOU:

In terms of inflation:

- Moderate inflation is associated with economic growth, while high inflation can signal an overheated economy.

- So, although the media has painted inflation in a negative light, some inflation is actually good for the economy.

The Fed’s preferred measure of inflation is the Core Personal Consumption Expenditures (PCE) Index. The PCE measures prices paid by consumers across several categories. The Fed is actively trying to boost this inflation reading above 2%, despite it being stubbornly below that level for the last decade (the 10-year average of Core PCE Inflation is +1.6% Y/Y). What this means is that the Fed is letting inflation rise a bit, which again, is good for the economy.

In terms of the National Debt:

- Throughout the 20th century despite rising debt levels, the United States has grown dramatically more prosperous.

- A steady market for federal debt has been a blessing for the United States as it enables the country to tap capital markets when needed.

- This prosperity has underpinned the serviceability and sustainability of U.S. debt. It allows the United States unrivaled fiscal flexibility today to meet challenges like stimulus to help citizens and businesses deal with recent Coronavirus crisis.

- The attractiveness of US debt has remained high as the world’s most liquid and deep market at $20 trillion+.

- No other country rivals the US for issuing a global safe-haven asset. As a result, the US dollar has remained quite strong during the past 30 years.

While high, by historical standards, the country has grown out of debt levels this high before and will likely do it again. In fact, over the past 30 years as government debt and spending have risen, interest rates have fallen dramatically.

Viewing interest costs through the lens of U.S. GDP confirms the current low-rate environment. Through the 1970s, net interest on the national debt equaled no more than 1.5% of GDP. By 1985 that cost had ballooned to more than 3% of GDP. But in 2020 net interest was back to 1.6%. On a relative basis, the cost of the national debt today is half its cost 10 years ago, and no worse than nearly half a century ago.

Despite recently rising interest rates, they are still near record lows, making the cost of borrowing very attractive. That could prove a boon, especially if the money is spent on investments, such as infrastructure, that can grow the economy in the future.

Should you wish to speak to a financial advisor about inflation and national debt, or another financial planning topic. please feel free to reach out to us.