In order to enhance your financial situation, it is crucial to reconsider the conventional notion of “winning the tax game” which involves approaches such as minimizing tax payments in the present year and receiving substantial tax refunds annually. It is important to recognize that adopting such strategies can often lead to adverse long-term financial consequences. This article aims to assist you in reevaluating your understanding of taxes and highlight tax pitfalls to avoid, improving your overall financial well-being. While each situation is unique, avoiding these tax pitfalls generally will put more money in your pocket and increase your spending power in your retirement years.

Tax Pitfall #1: Short-Term Focus

Many people become excited when they learn of tax-saving strategies that can lower their lifetime tax bill by tens or even hundreds of thousands of dollars. That excitement can quickly turn to confusion and frustration without taking the time to understand the intricacies of long-term tax planning.

Tax saving strategies such as Roth conversions and net unrealized appreciation (“NUA”) can save people a considerable amount of money over their lifetime, however both result in an upfront tax bill that can come as a surprise to the unprepared. These tax saving strategies act similarly to a “buy-now-pay-later” option that consumers have come to love, but in reverse. To take advantage of them, you must pay taxes in the year the transaction is made to get tax savings in future years.

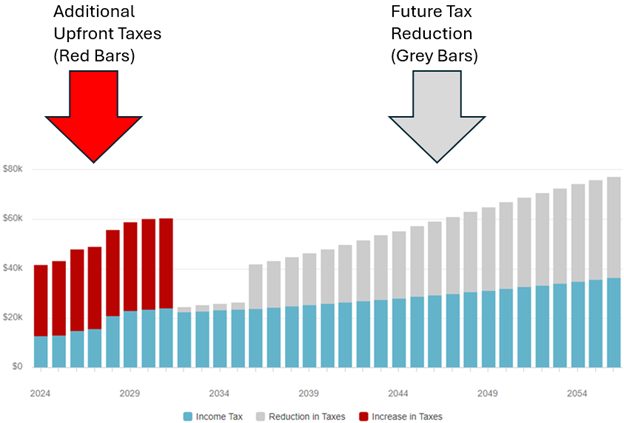

Each person’s financial situation is unique, but let’s look at Sally for example, who retired in 2023 at age 62. If Sally executed a $100k/yr Roth conversion from age 63 until age 70 it is projected that she would pay additional upfront taxes of $236,119 over those 8 years (the red bars below). Ouch – you can see how the upfront tax bill can be an emotional hurdle. However, when we zoom out to see the reduction in taxes over Sally’s lifetime (the grey bars below), the benefit is clear, as it saves her $367,144 in lifetime taxes (yes, that is net of the upfront taxes paid in years 1-8). What would you do in retirement with an extra $367,144 in your pocket?

It is crucial to prioritize long-term advantages when executing tax strategies. Failing to do so may result in excessive tax payments throughout your lifetime, hindering your ability to enjoy retirement to the fullest.

Tax Pitfall #2: Under-withholding

New retirees are often in the “sweet spot” to carry out tax-saving strategies such as Roth conversions and NUA mentioned above that increase one’s tax bill in the year of execution. The implementation of these strategies is likely to coincide with a huge change in the new retirees’ tax situation – their employer is no longer withholding taxes for them. If not properly planned for, the combination of a lack of tax withholdings coupled with an increase in taxes owed can catch even the most financially adept person off guard with a sizeable tax bill due.

There are simple ways to avoid these tax-time surprises, such as identifying where your retirement income is coming from and setting up sufficient tax withholdings from those sources upon retirement. This may include income from sources such as Social Security, pensions, and retirement account withdrawals. Another option is to make estimated quarterly tax payments.

Tax Pitfall #3: Over-withholding

Overpaying taxes during the year may lead to receiving a tax refund but is tantamount to providing the government with an interest-free loan. The IRS does not provide you with any interest payments for providing more than you had to during the tax year. Rather than over-withholding taxes, it is advisable to invest that money in an investment account or high-yield savings account to generate growth and earn interest.

Tax Pitfall #4: Overlooking the Power of QCD’s

While many retirees are aware of Required Minimum Distributions (RMDs), few realize they have a “superpower” available to them once they reach age 70½: the Qualified Charitable Distribution (QCD).

The pitfall here is simple but costly: taking a Traditional IRA distribution to fund your charitable giving instead of using a QCD. When you withdraw money from a traditional IRA and then write a check to a charity, that withdrawal is first counted as taxable income. Even if you itemize your deductions, you may not get the full tax benefit due to adjusted gross income (AGI) floors or the high standard deduction amounts updated for 2026.

Why the QCD Wins

A QCD allows you to transfer up to $111,000 in 2026 (indexed for inflation) directly from your IRA to a qualified charity. The beauty of this strategy lies in its “invisible” nature:

- Zero Tax Impact: The money goes straight to the charity and never hits your tax return as income.

- RMD Satisfaction: The distribution counts toward your Required Minimum Distribution for the year.

- Lowers your AGI: By keeping your Adjusted Gross Income lower, you may also reduce the taxation of your Social Security benefits and avoid higher Medicare Part B and D premiums (IRMAA surcharges).

If you are already giving to a place of worship, a local non-profit, or your alma mater, failing to use a QCD is essentially choosing to pay taxes on money you never intended to keep.

A Note on Reporting Your QCDs

It is important to remember that while a QCD is tax-free, the IRS doesn’t “automatically” know that your IRA distribution went to a charity. Your 1099-R form will likely show the full amount as a distribution, but it won’t specify that it was a QCD.

Pro Tip for 2026: To ensure you aren’t taxed on money you gave away, you must explicitly inform your tax preparer which distributions were made as QCDs. Without this communication, your preparer might inadvertently report the amount as taxable income, undoing all your hard work.

Conclusion:

Are you avoiding these tax pitfalls to minimize your lifetime tax bill? Want to learn if there are tax-saving strategies that you can implement? Schedule a no cost consultation with a member of our team at Runey & Associates.

This information is intended to be educational in nature and should not be construed as investment or tax advice. Each person’s tax situation is unique, and we encourage you to work with your tax professional when evaluating your own situation.